The 2023 H1 Northern European Data & AI Investment Landscape

The 2023 H1 Northern European Data & AI Investment Landscape

At J12, we back early-stage data & AI teams across Europe, but, in recognition of our home in Stockholm, we wanted to deep-dive into what’s been going on up here in the north. We hope you enjoy.

This report is for anyone that is curious to gain greater insight as to what is being built within data & AI in Northern Europe, and where the money is flowing.

The data relates to investment rounds that took place during 2023 H1, in companies building with or for AI, across the Nordics & Baltics.

🇸🇪 🇳🇴 🇩🇰 🇫🇮 🇪🇪 🇱🇻 🇱🇹 🇮🇸

(If you’re viewing this as an email, feel free to click “View in browser” above the title for a clearer reading experience.)

Quick disclaimer & clarifications:

This report is based on publicly available data, meaning some rounds may be missing and some information may be incomplete (such as when round size is unknown).

Rounds have been included if publicly available data suggests that they took place between 1st January 2023 and 30th June 2023.

The categorisation of investment rounds and companies is entirely based on (sometimes limited) understanding of what the company does - based on direct interaction and/or publicly available information.

If you feel something has been mis-categorised, or you know of a round that is missing altogether, please contact nordicaiweekly@substack.com to share what you know —> together we can improve the data.

Categorisation

We include investment rounds in companies that are either AI Enablers or AI Applications. Where the following definitions apply:

AI Enablers

Companies providing software infrastructure and tooling that enables others to build models and applications. We split these enablers into three sub-categories:

Data infrastructure - providing the underlying infrastructure and tools for collecting, managing, and working with data at scale.

Developer tools - helping software developers automate and streamline the process of building, testing, and deploying applications.

MLOps - providing tools that help data scientists and machine learning engineers manage the entire ML lifecycle.

AI Applications

Companies building applications where AI is at the core of the product offering. Applications may be built on proprietary models, or on top of other models (or a combination of both), and are based on varying underlying technologies. For the purposes of this report we categorise companies as predominantly applying either:

Data & Predictive Analytics

Generative AI

Computer Vision & Remote Sensing

With this focus, it is important to note that a number of companies and investment rounds relevant to the AI stack have been excluded - for example those operating in the hardware layer (e.g. relating to microchips and semiconductors) are not included.

Lastly, no investment rounds have been identified in companies seen to be operating at their core in the model layer of the AI stack.

What we’ll cover:

Overview of investment activity

Country-by-country comparison

AI enablers vs. AI applications

Investment rounds worth knowing about

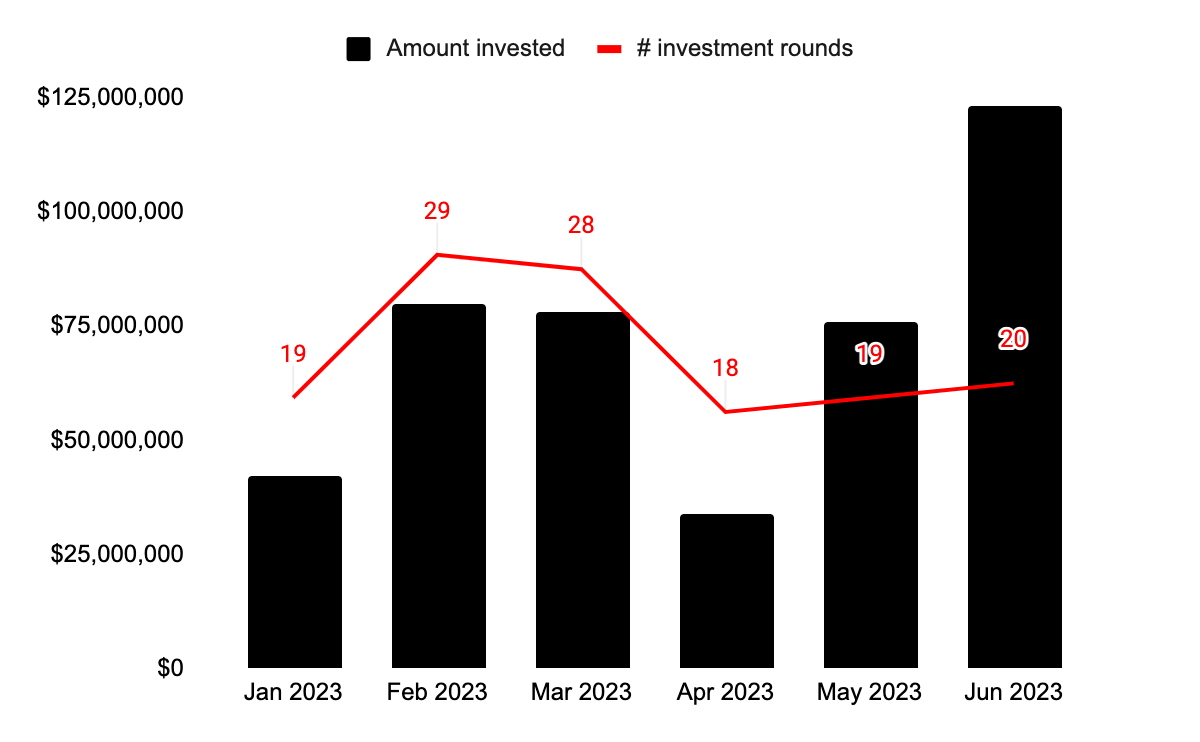

2023 H1 Nordic & Baltic Investment Activity

During the first half of 2023, $433m was invested across 133 different investment rounds in companies enabling or applying AI. Activity in terms of # of investments peaked around late Q1, however average investment sizes picked up through Q2 resulting in significantly more capital being deployed towards the end of the period.

This is out of a total of $3.52bn invested across 740 rounds in all companies. Thus, enablers and applications of AI represent:

18% of investment rounds

12% of capital invested

So, beyond where a lot of the hype and media attention may be, clearly the vast majority of capital continues to be deployed in companies that do not directly operate in the AI stack, or apply AI at core. Much activity continues to take place in non-AI companies across e.g. fintech, energy, healthcare, and manufacturing. Further down in this report we’ll explore which sectors are starting to see the most AI applications.

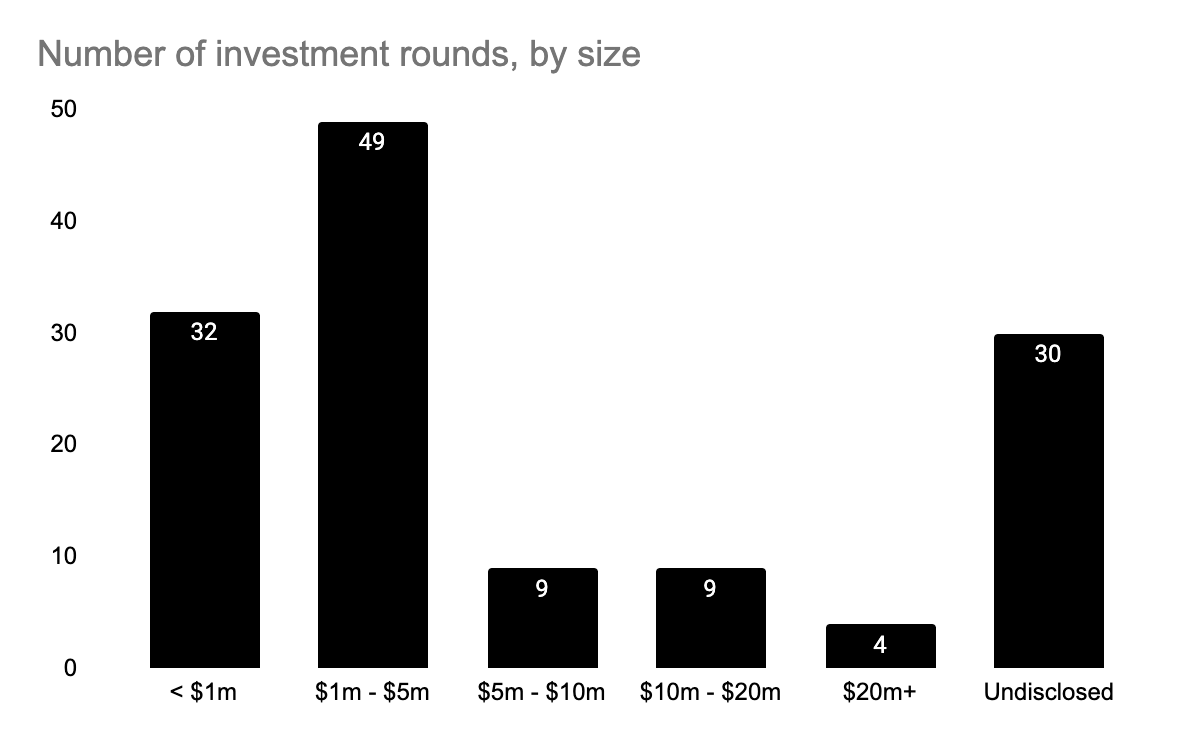

As one would expect, most activity has taken place in the earlier stages, with the majority of deals being rounds of less than $5m. In line with the market as a whole, larger rounds at Series A/B and growth stages have been few and far between.

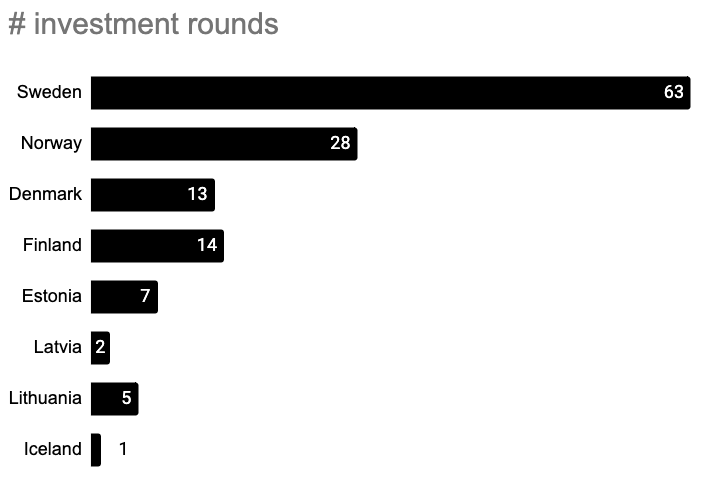

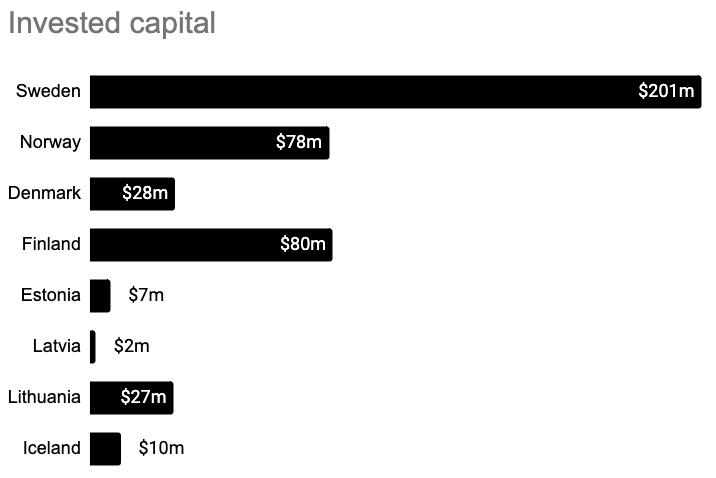

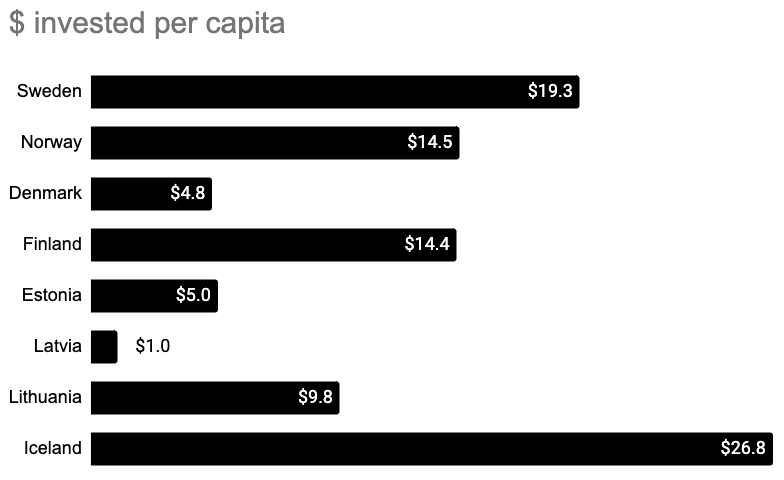

Breaking things down country-by-country

Sweden leads the way with 47% of investment rounds and 46% of invested capital deployed there. Norway follows strongly in terms of number of investments, but some larger rounds in Finland push it forward when it comes to invested capital. Lithuania too has clearly experienced a couple of larger rounds.

Iceland far outperforms relative to its population, although that is the result of one single sizeable investment rather than a cluster of strong activity. Estonia - which normally outperforms on a per-capita basis - ranks lower, suggesting either (i) a relatively quiet period of activity, or (ii) that most activity in the country lies outside of AI.

Interesting clusters of expertise can be seen in some locations (more details can be seen further down this report), for example in Norway where there is a flourishing market of robotics companies with 1X, wheel.me, and Blue Ocean Robotics raising $49m between them and thus accounting for 63% of the capital invested in the country. In Finland, there appears to be region-leading quantum computing capabilities, with Algorithmiq and Quanscient leading the way.

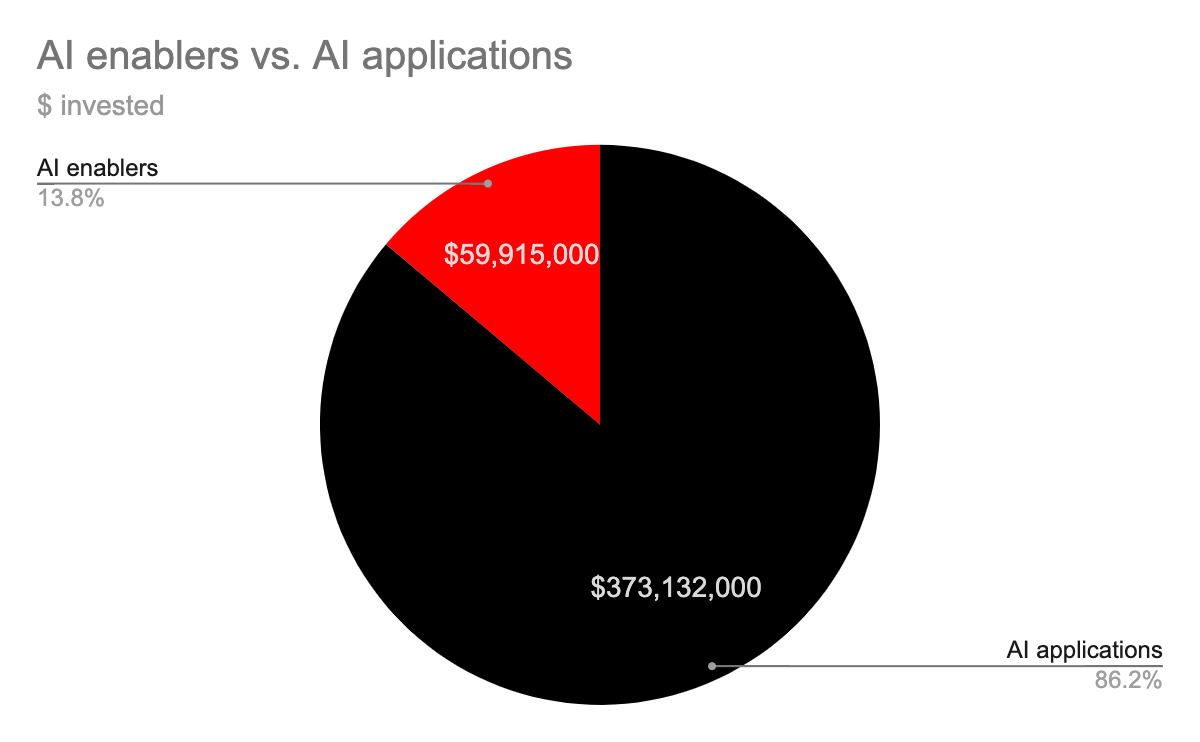

Enablers vs. applications

The most active part of the AI stack is clearly in the application layer, with the vast majority of invested capital being deployed into companies applying AI in some shape or form. Only 13 investment rounds (of the total 133) were in companies providing the software infrastructure and tooling that enables others to build models and applications.

* It is also worth noting the absence of any investment rounds in companies operating in the model layer of the stack - where the core product offering is the model itself (e.g. as OpenAI or Mistral AI). At least for now, it does not seem to be the focus of teams in the region to compete there. *

Below, we’ll look further into each of these two categories.

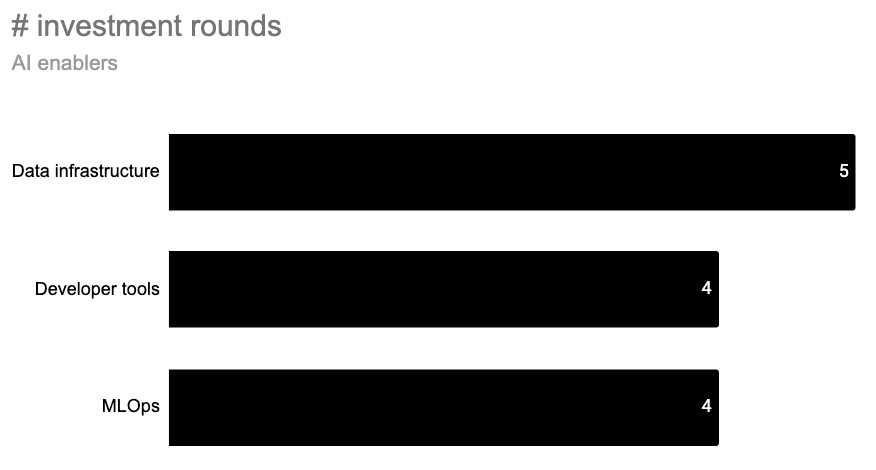

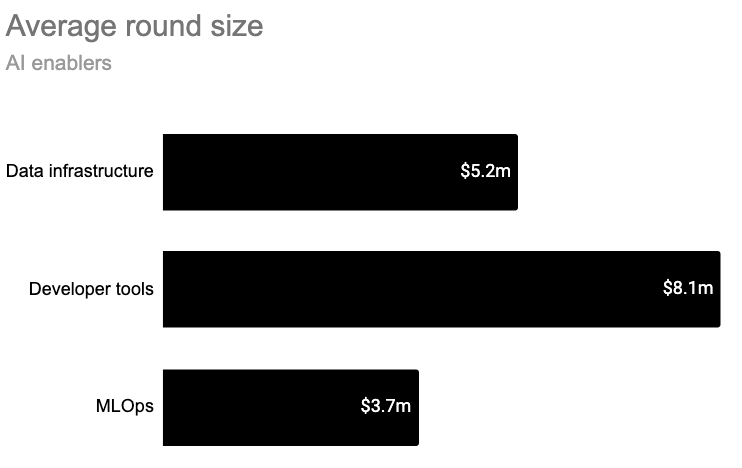

AI Enablers

Across the relatively few investments in AI enablers, there is an even distribution between the sub-categories. The greater capital deployed and larger average round sizes in data infrastructure and developer tools suggests that currently there may be greater maturity and later-stage opportunities in those spaces as compared to MLOps tooling.

* Average round size only takes into account investment rounds where round size was disclosed *

Data infrastructure companies are, for example, building products that enable data quality management (e.g. LiTech), enable the deployment of data pipelines and the scaling of infrastructure (e.g. Twirl), or that enable the modern data stack in enterprises (e.g. Wayfare.ai).

Within developer tools, we see companies optimising DevOps and cloud costs (e.g. Cast AI), enabling deployment in Kubernetes (e.g. Rig.dev), or providing no-code platforms (e.g. Formaloo).

Addressing MLOps, companies are providing model optimisation SDKs to deploy deep-learning (e.g. EmbeDL), collaborative ML platforms (e.g. Hopsworks), or federated learning platforms (e.g. Scaleout).

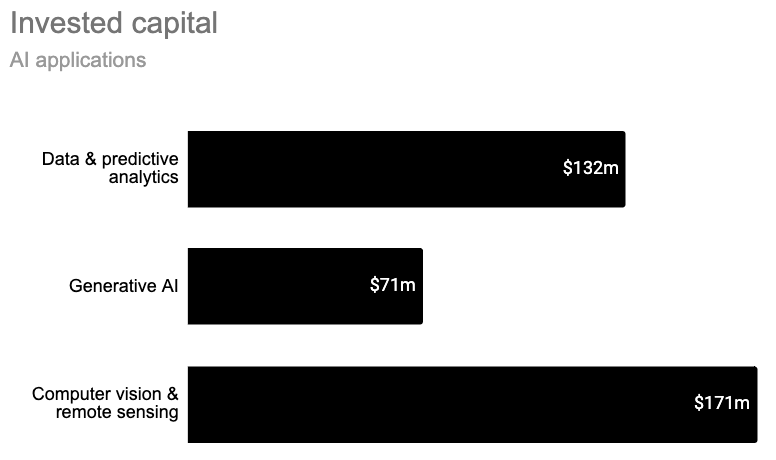

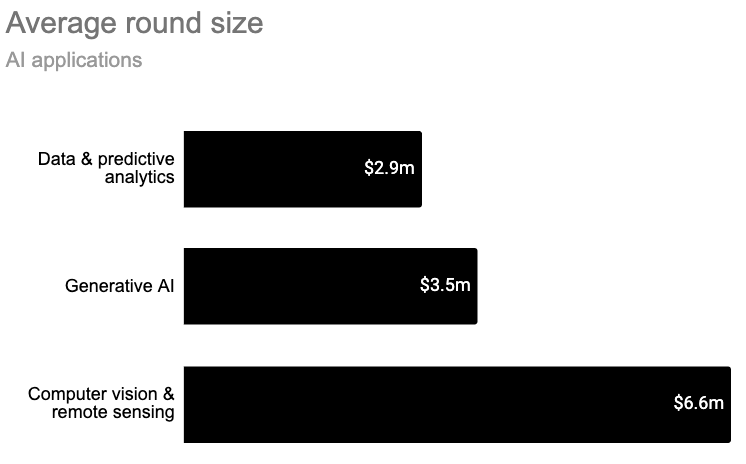

AI Applications

We can start by categorising applications based on their primary underlying technology.

* Obviously, most products use a combination of AI technology in order to power their applications, but here we attempt to categorise based on what may be considered most core. *

* Average round size only takes into account investment rounds where round size was disclosed *

For all the hype and attention, generative AI applications still lag behind those based on more traditional machine-learning models that analyse data and make predictions, or those based on computer vision technology. That said, genAI is likely the category with by far the most growth, and it will be interesting to follow how these areas develop in future periods.

Within data & predictive analytics applications, there are many companies making predictions & forecasts (e.g. machine maintenance, healthcare interventions, or retail demand), performing optimisations (e.g. energy performance, or personalised sound), and providing analytics & insights (e.g. in waste management, accounting, and sustainability).

Within computer vision & remote sensing applications, there are a range of companies across healthcare (e.g. diagnosis of skin conditions, eye screening, and radiotherapy), various monitoring use cases (e.g. infrastructure, agriculture, and forestry), and broadly within robotics.

Within generative AI, there are a broad range of use cases, but particularly evident activity within productivity tools (e.g. note-taking, email automation, and content creation), legaltech (e.g. navigating patent or compliance processes, or contracting), and education (e.g. improving content creation, knowledge sharing, and employee training).

Companies building upon computer vision & remote sensing technologies have typically raised around twice as much in their investment rounds, as compared to more ML and genAI based companies. This, though is likely a consequence of these companies often having hardware and/or robotics elements, and thus higher capital requirements.

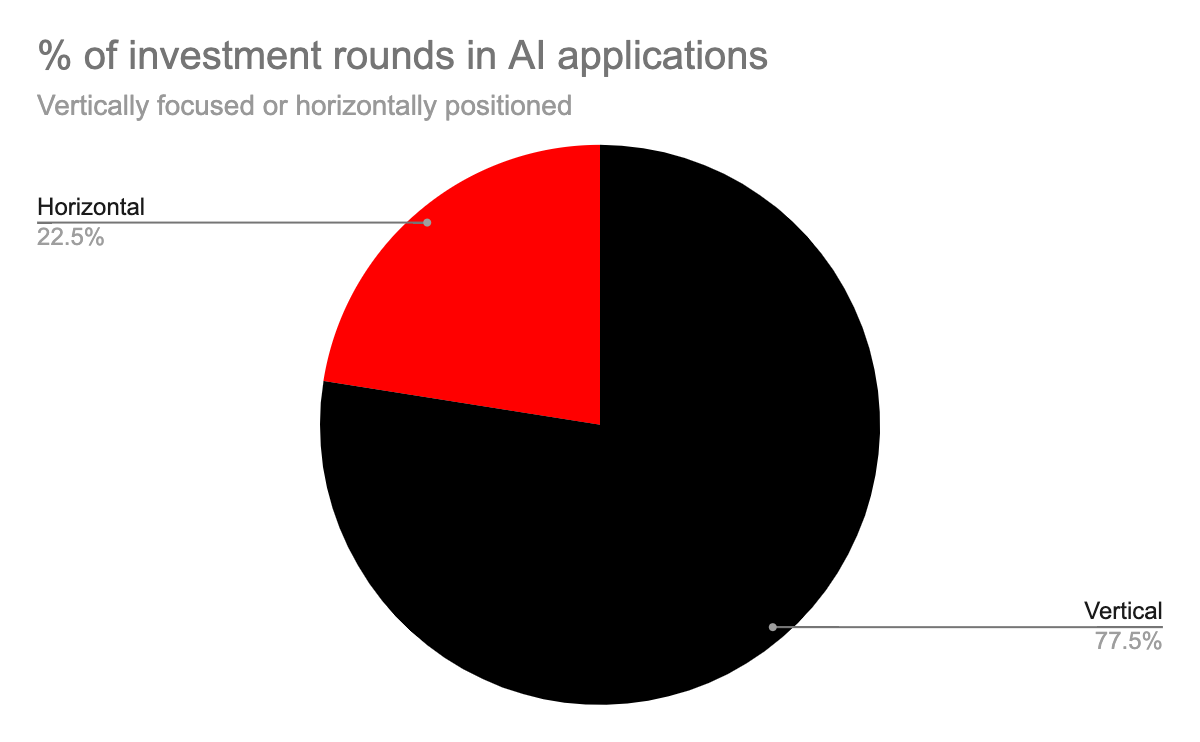

Vertical vs. horizontal applications

Looking at the application space, we can further try to break it down as to whether companies are offering solutions that are more vertically-focused, or horizontal in their positioning. Vertical solutions are those that are tailored towards a specific industry or domain, whereas horizontal solutions provide a broader offering that can be applied across a range of industries and use cases.

During the first half of 2023, more than two-thirds of investment rounds in AI applications were in companies with a more vertically-specialised positioning. When it comes to capital invested, the picture is much the same, with 75% of $ invested going to vertical applications. This resonates well with the view that there is potential advantage to be gained through (1) deep domain expertise, (2) the ability to leverage industry-specific data to fine-tune models or establish proprietary datasets, and (3) a targeted market focus that may enable more efficient distribution.

Noteworthy rounds

The 10 largest rounds

🇸🇪 Neko Health: Preventative healthcare via full-body scans backed by AI software - helping doctors detect skin conditions, cancer, cardiovascular disease, and diabetes, among other metabolic syndromes. Raised $65.04m from Lakestar, Atomico, and General Catalyst. #application #computervision&remotesensing #vertical #health

🇸🇪 Sana: Learning platform that empowers organisations to find, share, and harness the knowledge they need to achieve their missions. Raised $28m from Workday Ventures and New Enterprise Associates. #application #generativeAI #horizontal

🇳🇴 1X: Androids built to be as strong, gentle, and nimble as humans, in order to meet the world's labour demands. Raised $23.5m from OpenAI Startup Fund, Tiger Global Management, Alliance Venture, Sandwater, and Skagerak Maturo. #application #computervision&remotesensing #generativeAI #horizontal

🇱🇹 Cast AI: AI-driven cloud optimisation platform that slashes cloud cost, optimizes DevOps, and automates disaster prevention. Raised $20m from Creandum. #enabler #developertool

🇫🇮 Nosto: Commerce Experience Platform providing an integrated suite of data-fueled personalisation and merchandising solutions. Raised $16m from Mandatum Asset Management, Eurazeo, Tesi, OpenOcean, and Wellington Partners. #application #data&predictiveanalytics #vertical #retail

🇫🇮Algorithmiq: Developing advanced quantum algorithms to solve complex problems in life sciences. Raised $14.98m from Inventure, Tesi, and Presidio Ventures. #application #data&predictiveanalytics #vertical #lifesciences

🇳🇴 wheel.me: Robotics and IoT company that helps people improve the way they live and work by enabling “everything” indoors to move effortlessly on smart wheels. Raised $14.25m from MP Pensjon, Ferd Capital, Emerald Technology Ventures, and Idekapital. #application #computervision&remotesensing #horizontal

🇫🇮 Aibidia: AI, data, and automation-driven transfer pricing management platform. Raised $14.14m from DN Capital, FPV Ventures, Global Founders Capital (GFC), and Icebreaker. #application #data&predictiveanalytics #vertical #compliance

🇸🇪 Evroc: A secure, sovereign, and sustainable hyperscale cloud with best-in-class services and developer experience. Raised $14.14m from EQT Ventures and Norrsken VC. #enabler #datainfrastructure

🇳🇴 Blue Ocean Robotics: Developing, producing and selling professional service robots primarily in pharmaceutical, hospitality, and other global markets. Raised $10.84m from Nordic Eye. #application #computervision&remotesensing #horizontal

10 earlier-stage ones to watch 👀 (excluding J12 companies)

* There are many promising companies beyond those listed below, but these represent an interesting cross-section worth following. I have, for example, curated this list looking beyond companies in the J12 Ventures portfolio. *

🇸🇪 Supernormal: Automatically transcribing and writing your meeting notes. Raised $10m from EQT Ventures, ByFounders, Balderton Capital, and Acequia Capital. #application #generativeAI #horizontal #productivity

🇩🇰 Rig.dev: The open-source application platform for Kubernetes - build, manage and scale cloud native applications without overwhelming your engineers with the complexity of Kubernetes. Raised $2.18m from ByFounders, NP-Hard Ventures, Dreamcraft Ventures, Tiny VC, The Nordic Web Ventures. #enabler #developertools

🇸🇪 Fever: Energy flexibility platform that optimises market performance, capacity modelling, and asset orchestration - powering the smart electrical grid of the future to enable a sustainable world. Raised $1.55m from La Famiglia VC. #application #data&predictiveanalytics #vertical #energy

🇫🇮 Quanscient: Next generation Simulation-as-a-Service platform utilising quantum computing and state-of-the-art algorithms. Raised $3.78m from Maki VC. #application #data&predictiveanalytics #vertical #engineering

🇪🇪 Value.Space: Combining InSAR technology, AI for pattern recognition, predictive analytics and satellite imagery to conduct assessments for commercial properties and infrastructure globally to improve risk assessment, deformation identification and disaster prevention. Raised $2.3m from BADideas.fund, Inventure, Superangel, Specialist VC, Lemonade Stand, and AS Amalfi. #application #computervision&remotesensing #data&predictiveanalytics #vertical #insurtech

🇩🇰 Reshape Biotech: Integrated hardware and software platform digitising microbiology experiments and enabling lab automation at scale. Raised $8.1m from ACME Capital, Funders Club, and Y Combinator. #application #computervision&remotesensing #vertical #biotech

🇱🇻 Trace.Space: Enabling engineers to develop complex products 10x faster with AI-enhanced requirements management. Raised $1.5m from Fiedler Capital, Change Ventures, Foreword VC, and Tiny VC. #application #generativeAI #vertical #industry4.0&manufacturing

🇩🇰 Teton: Using computer vision to support care staff in providing the best care for their patients. Raised $5.3m from Plural and PreSEED Ventures. #application #computervision&remotesensing #vertical #health

🇳🇴 We Are: Using AI to create immersive learning experiences. Raised $1.04m from Skyfall Ventures and Sondo. #application #generativeAI #horizontal #education

🇩🇰 Wayfare.ai: Platform enabling the modern data stack in enterprises and regulated industries. Raised an undisclosed amount from PreSEED Ventures. #enabler #datainfrastructure

Very insightful 💡